Fed is showcasing its full powers, using its money printing machine as the wand in the face of an economic disaster due to the corona virus impact. Apart from buying unlimited government bonds, the Fed is backstopping loans of all kinds, buying corporate bonds, municipal bonds and also in its latest move, junk bonds. The central bank is now the single largest force moving markets and this is scary to say the least.

The extent of Fed money printing could touch USD 10 trillion, which is 50% of US GDP and this is just a bailout.

Along with the Fed, the US government is spending USD 2 trillion to bailout the economy with more spending to come. The supply of USD in the system has many implications for investors and most of the implications are negative.

The implications include, weak USD that can threaten its status as the worlds’s reserve currency. The US runs a current account deficit as well as a fiscal deficit, the twin deficits are often cited as a major factor for economic weakness in emerging currencies, but the USD has been able to maintain its reserve status given its significant presence in the world economy and need for governments to hold USD as reserves.

A ballooning US debt to GDP ratio, rising current account deficit, weak economy and deflationary conditions could severely impact capital flows and lead to USD weakening substantially. Excessive money printing by the Fed, if it produces no results of long term sustainable growth will further impact the attractiveness of the USD.

The repercussions of a sustained USD weakness will be felt across the world, and there would be a search for other assets that are seen as safe haven. US treasuries, generally seen as safe haven, would lose its lustre as investors shun US debt, which will be in oversupply at artificially low yields held by the Fed.

On a positive note, emerging markets like India could see better flows as money moves away for USD assets into growth economies that have a strong domestic consumption flavour.

Long Period of Economic Weakness

Too much use of antibiotics makes the body resistant to fight viruses and also weakens the body considerably leading to more and more infections. Similarly, any sign of trouble in the economy is being dealt with the antibiotic of fiscal and monetary stimulus, first started by the Fed and now embraced by governments and central banks across the globe.

The coronavirus has hit global economies at a time when they were most vulnerable, with China the world’s second-largest economy, seeing growth slow down sharply to 6% levels from high double-digit growth. Eurozone economy was weakening on the back of weak global trade while India’s growth had plummeted to below 5%, from 7% levels seen a couple of years ago. India is facing a slowdown in domestic demand and weak export growth. Japan was limping with low inflation and weak growth.

The US was the only economy that was seeing strength with unemployment at record lows, consistent job creation, and strong corporate earnings. However, the US too felt the effect of China slowdown and the trade war, prompting the Fed to change its stance from normalizing rates to cutting rates.

Economic weakness in all the economies was despite unprecedented fiscal and monetary easing post the 2008 financial crisis, which saw governments cutting loose fiscal ammunition and central banks pumping in huge amounts of liquidity at record low rates. At that time, economies were able to come out of the crisis slowly but the defenses against further shocks weakened.

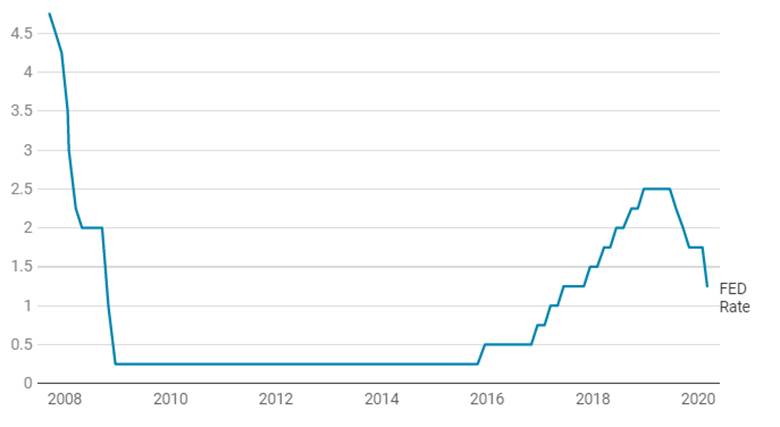

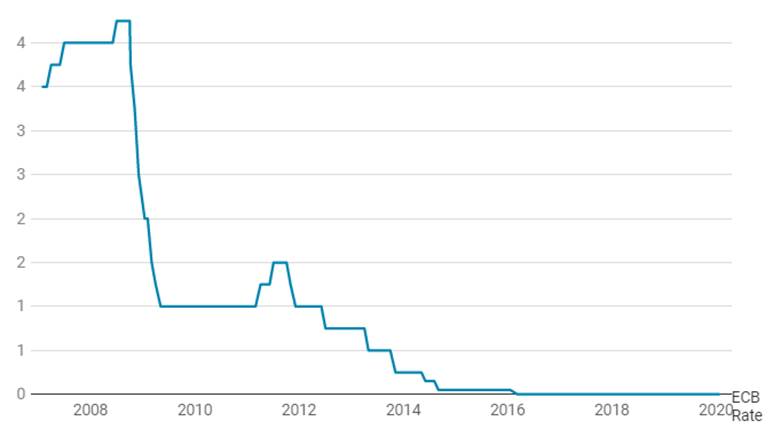

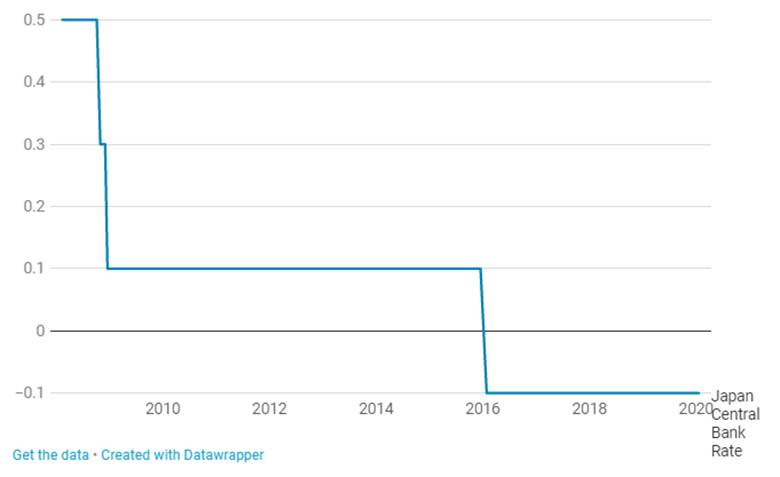

Government debt ballooned, inflation refused to pick and rates stayed at record lows. Fed took 10 years for the first-rate hike since 2008 while ECB has not raised rates since. Japan has been on stimulus for 30 years with no results.

Japan Inflation Growth (%)

Eurozone Inflation Growth

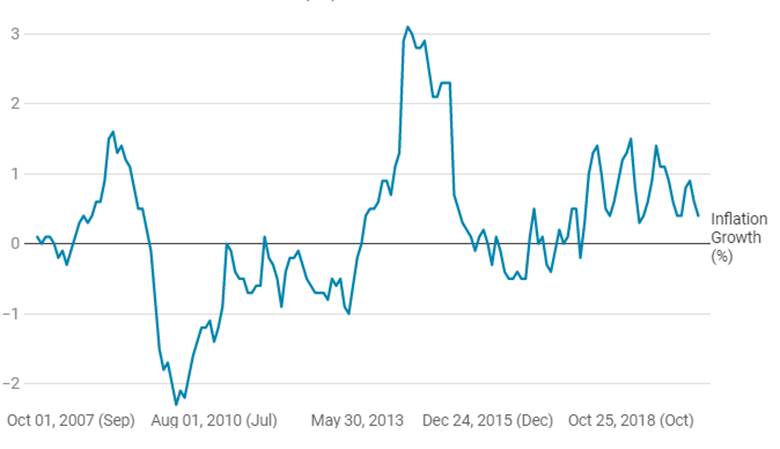

US Inflation growth (%)

In the fight against the coronavirus, governments are increasing debt for fiscal stimulus while central banks are lowering rates and pumping in liquidity. When the virus issue goes away, economies can see an uptick in growth largely because of the low base effect but the economies will be weaker with high government debt and low rates that hurt an aging population that cannot afford rising costs despite headline inflation at record lows.

When the next shock happens, which will happen given the way the world is affected by climate change, economies will be left almost defenseless and no amount of fiscal and monetary stimulus will work.

It is high time that economies build up defenses to shocks through prudent policies, leaving enough space for stimulus to work when it’s required.

Quantitative Easing is essentially a monetary policy tool used by central banks globally to inject liquidity directly into the system. The US Federal Reserve System had undertaken quantitative easing (QE) following the global financial crisis of 2007–08 and mitigated some of the economic problems since the financial crisis. To some extent, QE helped global economies to recover from the recession which was witnessed during the 2007-08 financial crisis. But however, the growth rates reported by the developed nations have not achieved what they had reported prior to the financial crisis. Excessive liquidity will lead to depreciation of the currency and in turn, hurts countries that highly depended on imports. QE is not the solution every time when the economies slow down, otherwise, the global economy currency will slowly shy away from the intrinsic value. Economies internally should have the capacity to absorb the liquidity provided by the central bank in order to spurt demand levels, given the lower demand levels and high liquidity could affect macro indicators of the country in long run.

As per Reuters report, mature markets total debt now tops USD 180 trillion or 383% of these countries combined GDP, while in emerging markets it is double what it was in 2010 at USD 72 trillion, driven mainly by a USD 20 trillion surge in corporate debt. Global government debt alone is set to break above USD 70 trillion. Emerging markets are also loading up with excessive levels of Debt to GDP, China’s total debt to GDP is above 300%. Government debt to GDP of China stood at 55% and India stood at 70%. Another potentially risky trend is that the amount of emerging market hard currency debt (debt sold in a major currency like the dollar) that can become hard to pay back if a crisis hits a local currency’s value.

The Covid-19 virus spread is now global and this can have a long-lasting effect on markets even if the virus is contained in a few months. The reason is that global economies including India are already weak and central banks have maintained an easy stance since 2008, proving that their resources are limited. Given this scenario, there is no visibility on growth going forward even with government stimulus.

The Fed cut rates as an emergency measure to combat the Corona Virus effects on the Economy. The rate cut yesterday, the 3rd of March 2020, drove down US Treasury yields to record lows of below 1% and also took down the USD against the Yen and pulled down US equities.

The Reserve Bank of Australia cut interest rates on Tuesday in response to the growing threat from the coronavirus epidemic to the global economy.

The markets took the Fed rate cut as an affirmation that the virus will have a major impact on economies and corporate earnings. Global economies were already weak and with this virus and fall in oil prices, major economies and oil economies will see a huge impact on growth. Recession is not far away as seen by bond yields that are negative in Eurozone and Japan and at record lows in the US.

FED Rate Since 2007

ECB Rate (%)

BOJ Rate (%)

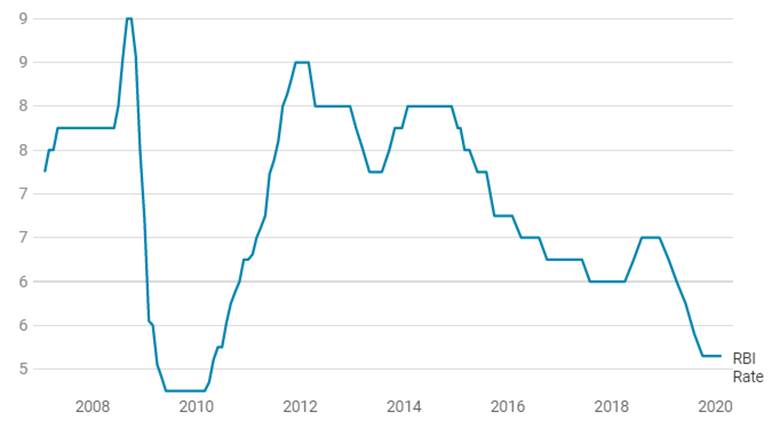

Reserve Bank of India Rate (%)