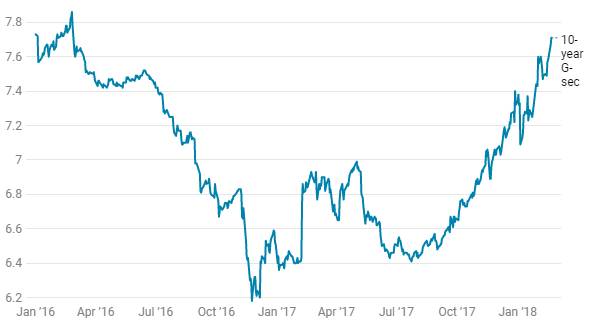

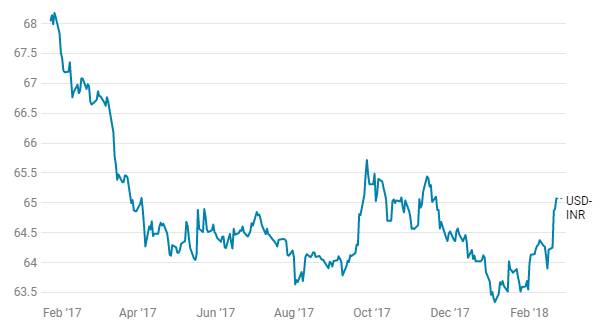

India 10-year G-sec bond yields rose to 2 years high at a level of 7.77%, while USD-INR breach the level of Rs 65 to the USD. 10year Gsec yields have risen by 60bps since January 2018 while the INR is down by 1.8% month on month. Why are 10-year gsec and INR tanking and what should market participants and investors do now in terms of positioning their investments?

The rise in 10 year gsec yields is explained by multiple factors of worries of banks staying away from bond markets for reasons why banks are staying out of bond markets, rise in 10 year US treasury yields that are a few basis points off 3%, worries of FII selling bonds on a tanking INR and rise in bonds yields and Fed and RBI Policy minutes.

The INR has not followed a broad emerging market trend of currencies weakening against the USD. Apart for Indonesian Rupiah and INR, other EM currencies have been broadly positive against the USD. FII’s too have not been net sellers of INR Bonds this month. Forward premia is stable around 4.5% levels.

INR fall is largely to do with unwinding of overbought positions as the currency was one of the best performing currencies before the fall. The fact that the Chinese Yuan is showing a sharp uptrend is also forcing players to shift from INR to Yuan.

Given the broad market sentiment, every long position in 10 year Gsec or short position in USD/INR can go deeply negative in a very short span of time. Gsec market liquidity too is extremely low and small selling pushes yields up very quickly. In the short term, it is best to play the trend with very small positions or stay away fully from the market till stability emerges.

In the longer term, fundamentals surrounding both the 10 year gsec and INR are strong with India showing strong economic growth, falling fiscal deficit and stable inflation expectations. Read our note on Union Budget 2018-19 for an analysis of Indian macros. The rise in gsec yields and fall in INR can be used to build long positions. RBI has built up fx reserves to stem any short term currency volatility with fx reserves at USD 420 billion, a record high and with a USD 29 billion forward purchase position.

10-year G-sec yields are rising as the market expects higher inflation going forward due to higher crude prices, MSP increases, fiscal slippage and Pay Commission implementation, while INR is falling due to hawkish Federal Reserve minutes, recent PNB scam has also put pressure on INR.

Rising Inflation Expectations and RBI, Fed Policy Minutes

In last few weeks bond yields had risen sharply as the market expects higher inflation due to shift in government policies from supporting consumers to supporting food producers, which will increase the MSP prices. India 10-year G-sec yields had also risen due to global cues, UST yields have risen sharply over the last few months, the reasons include US corporate numbers coming out much better than the market expectations, strong US economic data with US economy expanding by 2.6% in Q4 2017 signaling that the economy remains solid and consumer prices in the US increasing by 2.1% (Y-o-Y) in January 2018, the same as in December 2017 but above market expectations of 1.9%. Expectations are that the US Fed is going to tighten rates faster than expected, leading to a spike in US treasury yields.

10-year G-Sec Movement

USD-INR Daily Movement

RBI February 2018 policy minutes suggest MPC members are concerned about rising inflation, but they voted for status quo because economic growth is reviving in India and it is in an early stage.Minutes suggest MPC members are concerned about inflation risk because of higher food and crude prices, government’s decision to increase spending in the agricultural sector. Fiscal slippage is also a key risk to inflation.

One of the MPC member Michael Patra voted for 25 bps rate hike, Patra said the near-term outlook for inflation is likely to breach of RBI inflation target and it is important to recognise that the expected easing of inflation in the second half of 2018-19 is largely statistical as the HRA effect wanes. A fiscal deficit target of 3.3% along with the promise of higher minimum support prices and the customs duty hikes will ensure that rising inflationary pressures get entrenched. Fixed income markets are telling us that we have fallen behind the curve.

Federal Reserve policy minutes suggest that improvement in the global economy and recently passed tax cuts have raised the prospect for solid growth and continued interest rate hikes. Officials suggested that tax cuts have increased the upside risk to inflation. Improvement in consumer spending and confidence are signs that the economy is moving along at a sustained pace. Almost all the Fed Reserve officials saw inflation moving up to the Fed 2% inflation goal over the medium term as growth remained above trend and the labour market stayed strong.

US 10-Year Bond Yields