RBI Policy Outcome & Q2Fy21 Earnings will Set Trend for Sensex & Nifty

Equity Markets Snapshot for The Week:- Minutes from the Federal Reserve and European Central Bank will be in the spotlight next week.

- Japan will publish current account figures.

- Domestic market participants will look out for RBI policy-meeting outcome & Q2Fy21 Corporate Earnings.

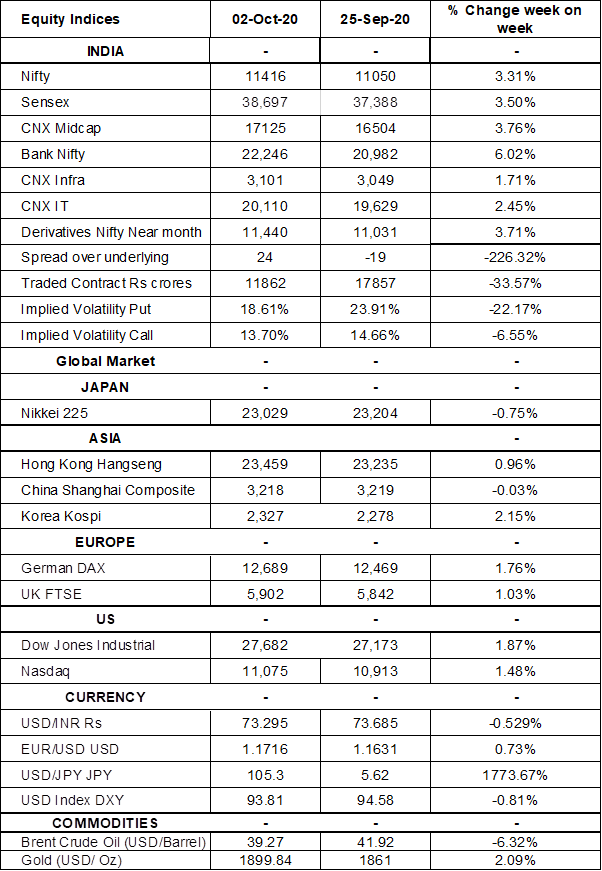

- Implied volatility (IV) for put and call at the money options stood at 18.61% and 13.70% levels respectively.

FIIs/FPIs have sold Indian equity shares worth Rs. 77.83 billion in September 2020 and sold shares worth Rs. 2.65 billion in October 2020 (till 03rd October 2020). Foreign Institutional Investors (FIIs) Derivative Statistics have shown a rise in the open interest across Index Futures, and Stock Options.

The Nifty Index futures witnessed rise in open interest by 33% for October series and fall in open interest by 26% for the November series. Implied volatility (IV) fell for call option and for put option in the last week. Fall in IV for call option and in IV for put option shows steady support for Nifty at present levels.

The BSE Sensex index jumped more than 600 points or 1.7% to close at 38,697 on Thursday amid hopes for a quicker economic recovery after India's government allowed states to reopen more non-essential businesses. In addition, the September PMI survey showed the country's manufacturing sector grew by the most in over eight-and-a-half years, with output increasing at the third-quickest rate in the history of the survey and new orders expanding the most since early-2012 boosted by a rebound in exports. Still, employment decreased for a sixth consecutive month. Economic data released on Wednesday showed India reported the largest current account surplus on record during the April 2020 to June 2020 period, while infrastructure output contracted at a faster pace in August 2020 and the fiscal deficit widened sharply. The IHS Markit India Manufacturing PMI surged to 56.8 levels in September 2020, the highest since January 2012, from 52 levels in August 2020, amid easing of COVID-19 restrictions. During last week, Sensex & Nifty surged by -3.5% & -3.31% respectively.

On global front, US indices opened on a negative note on Friday following the news on President Trump tested positive for Covid-19, however, markets closed on a positive note after the house speaker mentioned about striking deal on a new aid package. During the week, Dow Jones gained by 1.90%, Nasdaq rose by 1.48% and S&P 500 increased by 0.44%.

European indices rebounded in afternoon trading to close on a flat note on Friday. Coronavirus concerns continued to dent investors sentiment. US jobs report also weighed on investors sentiment. During the week, FTSE gained by 1% and DAX rose by 1.76%.

During the week, Brent Crude Oil declined by 6%, spike in coronavirus infections worldwide raised fears about fuel demand recovery.

Global Economy

The US economy added 661,000 jobs in September 2020, easing sharply from an upwardly revised 1.489 million in the previous month, and below market forecasts of 850,000. However, jobless rate dropped to 7.9% from 8.4% in August 2020.

Corporate profits in the US tumbled by 10.7% to an over four-year low of USD 1.59 trillion in the second quarter of 2020, compared to an initial estimate of an 11.8% decline. It was the sharpest decline in corporate profits since the last quarter of 2008, amid the coronavirus crisis.

The IHS Markit Eurozone Manufacturing PMI increased to 53.7 levels in September 2020 from 51.7 levels in the previous month.

Japan Manufacturing PMI was revised higher to 47.7 levels in September 2020, from a flash reading of 47.3 levels and compared to a final 47.2 levels in the prior month. The latest reading was the highest since February, as output fell at the weakest pace in seven months.

Japan's industrial production rose by 1.7% from the previous month in August 2020, easing from an 8.7% jump in July but slightly beating market expectations of 1.5%.

The Caixin China General Manufacturing PMI was little-changed at 53 levels in September 2020, slightly below market consensus of 53.1 levels, indicating factory activity maintained its recovery momentum in the wake of the COVID-19 epidemic.

The number of Americans filling for unemployment benefits rose by 837,000 in the week ended 26th September 2020, compared to an upwardly revised 873,000 in the previous period and slightly below market expectations of 850,000.

US crude oil stocks fell by 1.980 million barrels in the week ended 25th September 2020, the third consecutive week of decline and compared to market expectations of a 1.569 million rise, according to the EIA Petroleum Status Report.