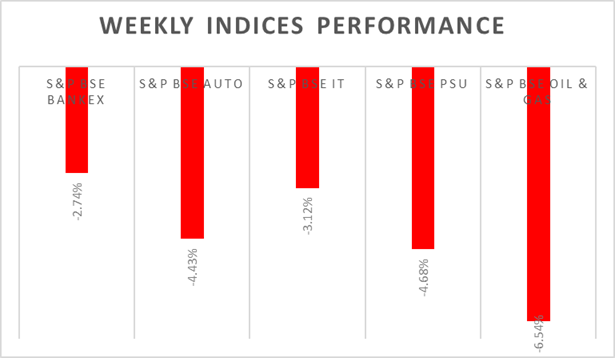

Sensex & Nifty were up 2.5% on Friday, snapping 7-day losing streak and rebounding from 6-month low levels. Global equities would continue to be volatile as the western continue to impose harsh sanctions on Russia amid Russia-Ukrain war, in the latest development US, Eurozone and Japan banned Russia from SWIFT transactions. Fresh sanctions are escalating the current issue and would impact global trade. On the other hand, markets are expecting a 25bps rate hike and mostly it has been discounted in both equities and bonds. But 50bps rate hike could lead to a knee-jerk reaction in markets. CME�s FedWatch tool shows probability of 50bps rate hike is at 9.5% compared to 50% above 2 weeks back.

Investors will watch out for developments in Russia and Ukraine matter, ECB policy-meeting minutes, OPEC+ meeting and US non-farm payroll data. China will release PMI levels GDP growth data. Domestic investors will watch-out for Q3 GDP growth data.

FIIs/FPIs have sold Rs. 333 billion in January 2022 and Rs. 311 billion in February 2022. Foreign Institutional Investors (FIIs) Derivative Statistics have shown a fall in the open interest (OI) in stock futures, index options, stock options and index futures.

Wallstreet indices rose consecutively for two trading days after witnessing sharp sell-off amid war tensions. Investors think Russia-Ukraine conflict could force Fed to for 25bps hike rather than 50ps rate hike. During the week, Dow Jones declined by 0.10%, Nasdaq gained by 1.28%, and S&P 500 closed on flat note. ��

European equity markets closed on a strong note on Friday, rebounding from a sharp sell-off in the prior session. European countries and US has banned few Russian banks from SWIFT payments. During the week, DAX down by 3.16% and FTSE fell by 0.32%.

Crude oil prices were under pressure as the tensions between Russia and Ukraine escalated and concerns of supply disruption supported the prices. Surprisingly US witnessed weekly rise in crude inventories.

Global Economy

The personal consumption expenditure price index in the United States rose by 6.1% (Y-o-Y) in January 2022, the highest since February 1982, and above 5.8% in December 2021.

The IHS Markit US Services PMI rose to 56.7 levels in February 2022 from 51.2 levels in the previous month and above market consensus of 53 levels.

US crude oil inventories rose by 4.515 million barrels in the week ended 18th February 2022, the most since October last year and following a 1.121 million increase in the previous period.

The number of Americans filing new claims for unemployment benefits decreased by 17,000 to 232,000 in the week ended 19th February 2022, from a revised 248,000 in the previous period and compared with market expectations of 235,000.

The German economy contracted by 0.3% on quarter in the last three months of 2021. It remains the first decline in GDP in three quarters, due to the fourth Covid-19 wave and another reinforcement of restrictions.

�