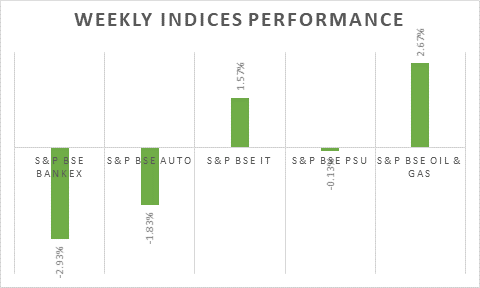

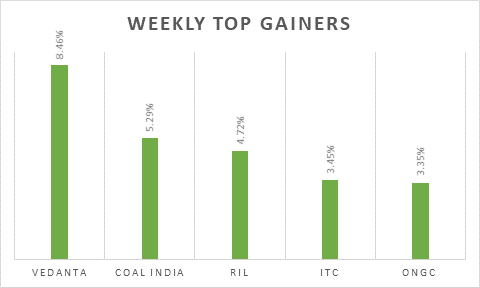

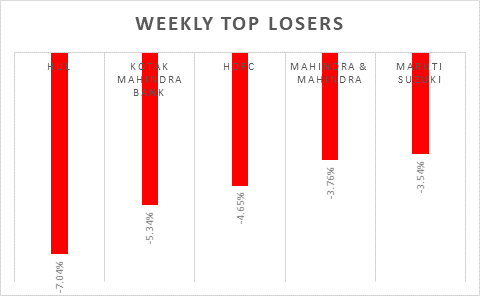

Sensex and Nifty closed the week on a negative note, driven concerns over higher inflation and ongoing geo-political issues. Going ahead market is expected to remain volatile due to F&O expiry and geo-political issues. Rising covid cases in China and lockdown also put some impact on market. Investors will remain watchful about Q4 corporate earnings and forthcoming RBI MPC meeting outcomes. Market eyes on policy rate hike possibility.

FIIs/FPIs have sold Rs. 355 billion in February 2022 and Rs. 415 billion in March 2022 (as of 25th March 2022).

Wallstreet indices closed higher on Friday. Fed’s stance on inflation and further rate hike in coming May impacted market sentiment. During the week, Dow Jones gained marginally by 0.31%, Nasdaq rose by 1.99%, and S&P 500 up by 1.17%.

European indices performed mixed during last week. Market was cautious about Russia-Ukraine war. During the week, DAX declined by 0.74% and FTSE up by 1.07%.

Global Economy

The current account deficit in the US shrank to USD 217.9 billion, or 3.6% of the GDP in the fourth quarter of 2021 from an upwardly revised USD 219.9 billion in the prior period. The services surplus rose slightly to USD 49.9 billion from USD 49.8 billion in Q3, and the primary income surplus also went up to USD 48.2 billion from USD 41.9 billion.

US initial jobless claims fell by 28,000 to 187,000 in the week ended March 19th, from a revised 215,000 in the previous period and compared with market expectations of 212,000.

UK inflation rate increased to 6.2% in February of 2022 from 5.5% in January and above market forecasts of 5.9%.

The index of leading economic indicators in Japan, which is a gauge of the economy a few months ahead and is compiled using data such as job offers and consumer sentiment, was revised lower to 102.5 in January of 2022, compared with the preliminary reading of 103.7, and after a downwardly revised 103.

US crude oil inventories fell by 2.508 million barrels to 413.4 million barrels in the week ended March 18th, after a 4.345 million rise in the previous period and compared with market expectations of a 0.114-million-barrel increase, data from the EIA Petroleum Status Report showed.

Equity Indices | 25-03-2022 | 18-03-2022 | % Change week on week |

Indian Indices | - | - | - |

Nifty | 17153 | 17287 | -0.78% |

Sensex | 57362 | 57863 | -0.87% |

CNX Midcap | 29274 | 28977 | 1.02% |

Bank Nifty | 35410 | 36428 | -2.79% |

CNX Infra | 4921 | 4917 | 0.08% |

CNX IT | 36152 | 35643 | 1.43% |

Derivatives Nifty Near month | 17216 | 17325 | -0.63% |

Spread over underlying | 63 | 38 | 65.79% |

Implied Volatility Put | 17.57% | 22.79% | -22.90% |

Implied Volatility Call | 21.56% | 21.11% | 2.13% |

Global Market indices | - | - | - |

Nikkei 225 | 28150 | 26827 | 4.93% |

Hong Kong Hangseng | 21405 | 21412 | -0.03% |

China Shanghai Composite | 3212 | 3251 | -1.20% |

Korea Kospi | 2730 | 2707 | 0.85% |

German DAX | 14306 | 14413 | -0.74% |

UK FTSE | 7483 | 7404 | 1.07% |

Dow Jones Industrial | 34861 | 34754 | 0.31% |

Nasdaq | 14169 | 13893 | 1.99% |

Currency Market | - | - | - |

USD/INR Rs | 76.25 | 75.96 | 0.38% |

EUR/USD USD | 1.099 | 1.1051 | -0.55% |

USD/JPY JPY | 122.06 | 119.14 | 2.45% |

USD Index DXY | 98.8 | 98.23 | 0.58% |

Commodities Market | - | - | - |

Brent Crude Oil (USD/Barrel) | 112 | 108 | 3.70% |

Gold (USD/ Oz) | 1957 | 1934 | 1.19% |