Sensex & Nifty were up by 1.5% in last week close to crossing all time highs. On the macro front, RBI & Fed paused interest rate hike during June policy-meeting, domestic inflation is declining and well in targeted zone of RBI and trade deficit recorded at 5 months high as exports declined sharply. FIIs/FPIs domestic inflows stood at Rs. 465 billion YTD.�

In the coming week, investors will watch out for Fed chair speech, PMI readings and UK�s monetary policy decision. In domestic markets, 4 IPOs will take the spotlight and they will be raising close to Rs. 6.4 billion.

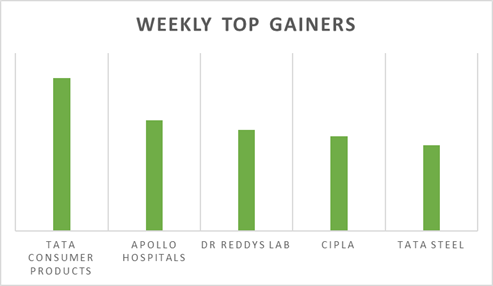

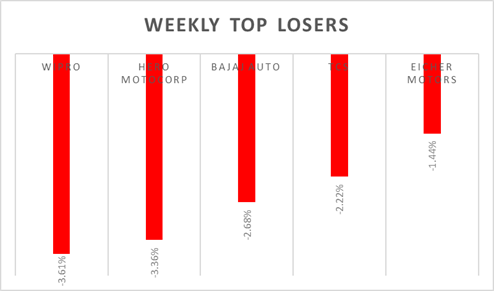

Equity Market Summary:

o �Dow Jones closed 100 points lower on Friday, the S&P 500 and the Nasdaq lost nearly 0.4% and 0.7%, respectively, as investors continued to assess the outlook of monetary policy for the Fed.

o Industrial production in the US went down 0.2% from a month earlier in May 2023, missing market expectations of a 0.1% increase.

o Fed left the target for the funds rate unchanged at 5%-5.25%, as expected, but signalled rates may go to 5.6% by year-end if the economy and inflation do not slow down more.

o European Central Bank raised interest rates by another 25 basis points during its June policy-meeting, bringing the rate on main refinancing operations to 4%, the highest level since the 2008 financial crisis, and the rate on the deposit facility to a 22-year high of 3.5%.

o China's industrial production advanced by 3.5% (Y-o-Y) in May 2023, easing from a 5.6% rise in April and slightly less than market forecasts of 3.6%.

o Bank of Japan kept its key short-term interest rate unchanged at -0.1% and that of 10-year bond yields at around 0% in its June meeting by unanimous vote. The board also made no changes to a 0.5% cap set for bond buying.

o Japan's trade deficit fell to JPY 1,372.5 billion in May 2023 from JPY 2,366.1 billion in the same period of the prior year, compared with market expectations of a JPY 1,331.9 billion gap.