IIP data for August 2019 showed a negative growth of 1.1%, the lowest in 6.5 years while passenger vehicle sales fell 24% year on year in September. The government effected a corporate tax rate cut last month, foregoing Rs 1.45 trillion of revenues while GST collection for September 2019 was Rs 910 billion down from over Rs 1 trillion seen a couple of months ago. Weak growth plus tax rate cuts would mean that government would have to revisit its fiscal deficit targets and may have to access the bond market to bridge revenue shortfalls.

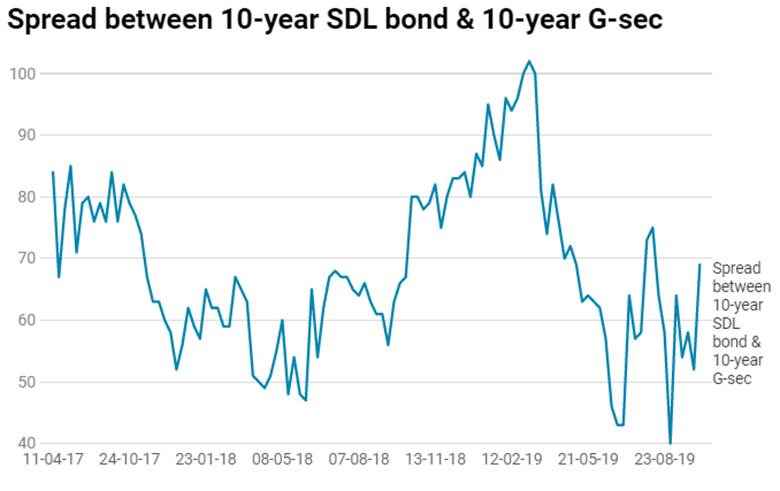

The government is looking to increase FII limits on bonds for absorbing supply if required and may also issue global bonds, which could help alleviate bond market’s worries on higher supplies. However, until the government clears its intention of bridging the fiscal gap, markets will tend to stay cautious.

CPI inflation for September is expected to come in higher month on month on the back of higher vegetable prices. Oil prices rose on Friday last week on news of an Iranian tanker blast.

The yield on the benchmark 10 year government bond, the 6.45% 2029 bond, rose by 5bps week on week on borrowing worries, higher inflation expectations and higher oil prices. However the yield is unlikely to trend much higher in anticipation of more rate cuts given weak growth and on demand from banks on the back of weak credit growth and excess liquidity. Credit growth fell to below 9% in September 2019 on lack of credit risk appetite among lenders given the issues facing the banking system in terms of weak banks and rising bad loans.

The bond markets will wait for developments on the borrowing front before starting to buy into the 10 year bond.

The OIS yield curve steepened on rate cut expectations with one year OIS yield falling by 5bps and 5 year OIS yield staying flat. The curve will continue to steepen, as markets will factor in more rate cuts while worrying about government finances.

Government spending is keeping liquidity at surplus of over Rs 2 trillion and RBI will look to issue CMB bonds to suck out excess liquidity.

The new benchmark 10 year gilt, 6.45% 2029 bond, saw yields close 5 bps up at 6.51% on a weekly basis. Benchmark 5-year bond, the 7.32% 2024 bond experienced yields up 5 bps at 6.32% and the 6.68% 2031 bond yield closed 10 bps up at 6.94%. The long tenure bond, the 7.63% 2059 bond yield closed 2 bps down at 7.12% levels.

One-year OIS yield came down by 3 bps to close at 5.03% while five-year OIS yield remained unchanged at 5.09%.

System liquidity as measured by bids for Repo, Reverse Repo, Term Repo and Term Reverse Repo in the LAF (Liquidity Adjustment Facility) auctions of the RBI and drawdown from Standing Facility (MSF or Marginal Standing Facility) was in surplus of Rs 2211.22 billion as of 11th October 2019. Liquidity was in a surplus of Rs 2717.03 billion as of 04th October 2019.