The cut off in the auction of a new 10 year benchmark government bond came in at 6.45% and the bond yield trended up by 1bps post cut off to close at 6.46%. The old 10 year benchmark bond, the 7.46% 2029 bond saw yields close at 6.66%, 20bps spread to the 6.45% 2029 bond.

The yield on the 6.45% 2029 bond will trend down sharply on the back of risk aversion in credit markets and on the back of more rate cuts by the RBI.

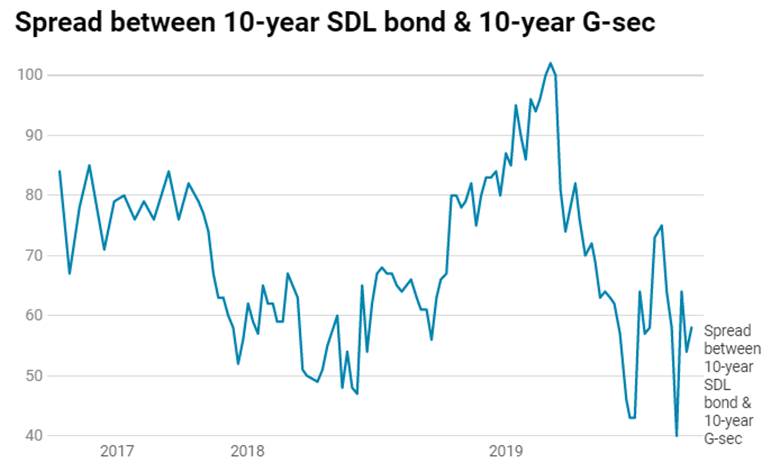

The stress in co-operative banks post PMC issue and on private sector banks like Yes Bank and Lakshmi Vilas Bank on issues of NPAs and corruption respectively is feeding into worries on the overall banking sector. There could be a flight to safety to stronger private sector banks and PSU banks, who will use excess liquidity to buy government bonds. Credit risk is high among lenders given the worries of more NPAs from real estate sector and also due to the general economic slowdown.

Globally too risk aversion is high with UST yields trending down sharply and Eurozone yields trending into negative territory. 10year UST yields closed down last week despite US unemployment rate hitting a 50year low in September.

Government bond yields are expected to trend down from highs on the back of RBI rate cut and easing of higher than expected borrowing worries. The government is also expected to issue a new 10 year benchmark government bond in replacement of the existing 10 year benchmark bond, the 7.26% 2029 bond, which has reached an outstanding of close to Rs 1.14 trillion.

RBI October policy review will see the RBI delivering a 35bps to 40bps rate cut given the weak economy and the need to push growth. Good monsoons, falling credit offtake (credit growth has come off to 10.26% levels in September against over 12% levels seen a couple of months ago) and stable oil prices despite Middle East tensions will prompt RBI to cut rates. Guidance too is expected to be accommodative given that both inflation and growth outlook are weak.

The bond market worries of higher than expected borrowing for the 2nd half of this fiscal year is likely to ease in October. The market is worried about the funding of the Rs 1.45 trillion fiscal gap that has arisen from the big bang tax rate cuts effected this month.

The government has not raised fiscal deficit or borrowing targets and is still awaiting incoming data on revenues. The higher compliance rate on tax rate cuts is also likely to see more taxes coming into the government’s kitty.

In case of revenue shortfall, the government can access global bond markets to fund extra borrowing. Higher domestic borrowings can be funded by increasing FII limits in bonds, as low to negative global bond yields can prompt FIIs to search for higher yields in INR Bonds.

The 10-year benchmark government bond, the 7.26% 2029 bond, saw yields close 5 bps down at 6.69% on a weekly basis. New 10-year benchmark cut-off yield stood at 6.45%. Benchmark 5-year bond, the 7.32% 2024 bond experienced yields down 15 bps at 6.27% and the 6.68% 2031 bond yield closed 10 bps down at 6.84%. The long tenure bond, the 7.63% 2059 bond yield closed 7 bps down at 7.10% levels.

One-year OIS yield came down by 2 bps to close at 5.08% while five-year OIS yield closed down by 4 bps to 5.09%.

System liquidity as measured by bids for Repo, Reverse Repo, Term Repo and Term Reverse Repo in the LAF (Liquidity Adjustment Facility) auctions of the RBI and drawdown from Standing Facility (MSF or Marginal Standing Facility) was in surplus of Rs 2717.03 billion as of 4th October 2019. Liquidity was in a surplus of Rs 1389.57 billion as of 27th September 2019.