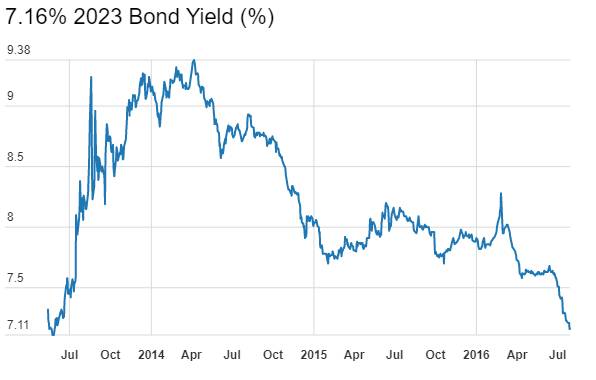

The benchmark ten year government bond, the 7.59% 2026 bond is trading at three year low levels of 7.16%. The yield of 7.16% is significant as the ten year bond that was issued on the 20th of May 2013, saw a cut off of 7.16%. The 7.16% 2023 maturity bond went briefly to around 7.10% levels before climbing all the way up to 9.25% levels as the INR depreciated to record lows against the USD in August 2013 prompting the RBI to hike rates and tighten liquidity. Chart 1 shows the movement in yields on 7.16% 2023 bond since the time it was issued in May 2013. The bond is currently trading at yields of 7.16%.

The current benchmark bond, the 7.59% 2026 bond has had a less volatile time since the time it was issued in January 2016, with yields touching highs of around 7.90% before dropping to current levels of 7.16%. Where will the yields go from here and what can potentially be the floor for the yield on this bond?

The factors driving the yield on the ten year bond are positive. The GST bill could be passed in this session of the parliament and that would be highly positive for the government to achieve its stated fiscal deficit target of 3% of GDP over the next couple of years. Inflation expectations are coming off on the back of good monsoons this year and oil prices staying at below USD 50/bbl is also contributing to inflation being kept on hold.

Markets would expect RBI to maintain a soft policy stance in its upcoming policy review and even if rates are not cut in August, signal would be more rate cuts ahead. The negative rates followed by ECB and BOJ coupled with Fed going slow on rate hikes will prompt the RBI to maintain an easy stance given potential dangers to the global economy on the back of Brexit.

The yield on the 7.59% 2026 bond is likely to go down to 7%, where it will pause to reflect on further economic data. The floor could be 7% or marginally below 7% for the bond yield though on rate cuts, if it happens in August, the bond yield could rise from lows on profit taking.

The government bond market saw bond yields falling last week on rate cut expectations. The 8.27% 2020 bond yield fell 5bps to close at 6.99% levels while the 7.59% 2026 bond yield closed down 9bps at 7.16% levels. The 7.88% 2030 bond yield closed down 13bps at 7.26% levels while the 8.13% 2045 bond yield closed down 16bps at 7.38% levels. Government bond yields will fall further on rate cut expectations.

OIS market saw one year OIS yields close flat and five year OIS yields close up by 7bps week on week. One year OIS yield closed at 6.50% while five year OIS yield closed at 6.49%. OIS yields will stay soft on easy liquidity conditions and on rate cut expectations.

Benchmark AAA corporate bond yields closed down last week. Three year bond yields closed down by 8bps at 7.53% levels with spreads down by 4bps at 51bps levels. Five year bond yields closed down by 10bps at 7.58% with spreads down by 3bps at 41bps levels while ten year bond yields closed down by 9bps at 7.86% with spreads flat at 57bps levels. Corporate bond yields will fall on rate cut expectations.

System liquidity as measured by bids for Repo, Reverse Repo, Term Repo and Term Reverse Repo in the LAF (Liquidity Adjustment Facility) auctions of the RBI and drawdown from Standing Facilities (MSF or Marginal Standing Facility and Export Credit Refinance) was in surplus of Rs 274 billion as of 29th July. The surplus was Rs 27 billion in the week previous to last. Government surplus was zero last week. Liquidity will stay easy on government spending.