Indian Rupee ended the week at Rs 71.86 levels against the USD after touching its fresh all-time low level of Rs 72.91 on Wednesday. The pressure eased on the India Rupee in the later part of the week after slowing inflation added to optimism that policy makers will take steps to stem a rout in INR. India’s annual retail inflation eased to 3.69% in August from 4.17% in July, the statistics ministry said on Wednesday largely helped by a smaller rise in food prices.

In a way to stem the INR slide, the government on Friday announced a plan to cut down “non-necessary” imports, ease overseas borrowing norms for the manufacturing sector and relax rules around banks raising masala bonds, or rupee-denominated overseas bonds.

Despite strong GDP growth, the rupee has weakened about 12% this year amid higher oil prices and an emerging market sell-off. This has widened India’s current account deficit and pushed its balance of payments into the red in April-June for the first time in six quarters and stoked inflationary pressures in the economy.

USD despite recovering on Friday ended the week on a negative territory. USD strengthened on Friday against all of the major currencies with euro leading the slide after every policymaker who spoke on Friday said more tightening beyond September is needed. Even FOMC voter and Fed President Brainard, who is traditionally a dove, suggested that the Fed could continue to raise rates beyond the long-term neutral rate. Evans, who is not a voting member of the FOMC, described the economy and labor market as very strong and suggested that 4 hikes for 2019 is still reasonable because he wouldn’t be surprised if inflation goes a little above 2%.

USD Index (DXY), which tracks the movement of the USD against six major currencies, fell by 0.46% on a week on week basis and is at a level of 94.93.

USD started the week on a lower note on Monday largely by a stronger pound in the wake of positive remarks on a Brexit deal from the European Union’s chief negotiator Michel Barnier. Further, the trade tension with China continues to weigh on market sentiment, as U.S. President Donald Trump warned that he would impose tariffs on USD 267 billion worth of Chinese imports, on top of an earlier promise of tariffs on USD 200 billion worth of Chinese goods.

Trade tensions escalated on Tuesday after reports suggested that China is planning to ask the WTO for permission to impose sanctions on the U.S. Beijing will formally place the request next week, as an apparent response to remarks from Trump. Chinese officials had previously stated that they would retaliate on any trade moves from Washington.

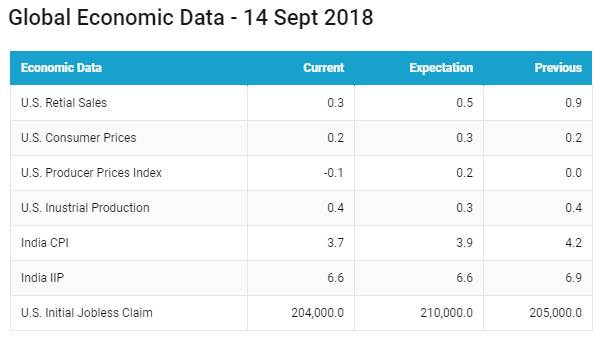

USD turned lower during mid of the week after the release of weak U.S. economic data and data suggested that the inflation pressures are easing in the economy denting expectations for a Federal Reserve rate hike in December. Consumer prices in the U.S. rose less than expected in August, increasing 0.2% compared to expectations for a gain of 0.3%. The slower pace of rising consumer prices in August, pushed the year-on-year increase in the CPI down to 2.7% from 2.9% in July.

Euro appreciated by 0.62% against the USD last week. The euro rallied after the ECB’s meeting on Thursday but on Friday, there were reports that some policymakers wanted a more cautious tone that suggested the risks were tilted to the downside. Data was also weak with the Eurozone’s trade surplus shrinking to its smallest level in 4 years in July.

The ECB kept its deposit rate at -0.40% and repeated that it expects its asset purchase program to end in December after halving it to 15 billion euros per month starting in October, from 30 billion euros at present.

Weekly Global Bond Market Analysis

US 10-year benchmark bond yields rose by 7 bps, UST yields closed at 3% after data showed economic growth was strong, which will keep the Federal Reserve in the path of rate hikes. Industrial Production rose 0.4% in August, the 3rdmonthly increase and the gain was above market expectation of a 0.3% increase. Investor confidence in the U.S economy rose to 14-year highs. The University of Michigan consumer sentiment index rose to 100.8 in September from 96.2.

Boston Fed President Eric Rosengren said he does not read much about a possible recession from the shape of the yield curve. Rosengren said he wouldn’t focus on the spread between the 10-year Treasury note and the two-year note, with quantitative easing occurring in Europe and Japan and while the Fed has its own big balance sheet, I think there are a lot of reasons to believe that that relationship is not constant. If an economy is growing very rapidly, inflation is picking up, and the yield curve is negative, I will still say we should be raising rates.

European Central Bank left its interest rates unchanged and reiterated its plan to scale down the size of its bond-buying program next month and end purchases in December. The ECB left its main lending rate, at 0%, while the paid-on deposits left overnight at the central bank remains at minus 0.4% and the rate on the marginal lending facility remains at 0.25%. President Mario Draghi said the central bank is on track to end bond purchases this year and raise interest rates next autumn.

Germany 10-year benchmark bond yields rose by 5 bps, as demand for safe-haven assets decreased after a report that Britain and the EU had made progress on the Irish border issue, a key hurdle in agreeing to a Brexit trade deal.

U.K 10-year benchmark bond yields rose by 8 bps, The Bank of England left its benchmark interest rate unchanged at 0.75% on Thursday, in line with market expectations. The BOE saw the U.K. economy broadly on track but highlighted that Brexit could still influence household and business spending in the future.

Italy 10-year benchmark bond yields fell by 7 bps, Greece 10-year benchmark bond yields fell by 22 bps, Spain 10-year benchmark bond yields rose by 1 bps, Portugal 10-year benchmark bond yields fell by 5 bps.

Emerging economies 10-year benchmark bond yields were mixed last week.

South Africa 10-year benchmark bond yields rose by 4 bps, Rating agency Moody’s said the outlook for South Africa credit rating is stable which means there is little chance of a downgrade this year, warned that a commitment to fiscal consolidation would be key to maintaining its rating.

Brazil 10-year benchmark bond yields rose by 13 bps, Political risk and a lackluster economic data will keep the pressure on bond prices, Brazil will go for the polls in October and there is no clear front-runner. The leader in the polls, Jair Bolsonaro, has yet to crack his baseline 20% support level. Brazil Institute for Geography and Statistics, IBGE, also lowered first-quarter output from 0.4% to 0.1%.

Australia 10-year benchmark bond yields rose by 2 bps, Russia 10-year benchmark bond yields fell by 38 bps, Indonesia 10-year benchmark bond yields fell by 2 bps.

US high-yield bond yields fell by 6 bps to 6.22% and Eurozone high-yield bond yields fell by 7 bps to 3.44%.