G-sec yield subdues despite rise in domestic inflation

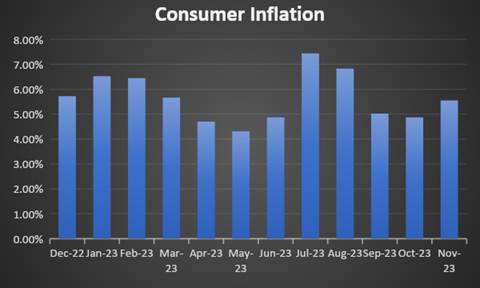

Domestic consumer inflation rose to 5.55% in November from 4.87% in the previous month. The rise in inflation driven by high food inflation. As per RBI�s inflation prediction, it will stay above 5% during Q3 & Q4 of the current fiscal year. Therefore, the market has already discounted the uptrend in inflation. Consequently g-sec inflation declined on a weekly basis as RBI has maintained status quo on policy repo rate.

System liquidity stood at Rs 443 billion of deficit as of 14th Dec. As RBI has not notified about the previously announced OMO sale, system liquidity is likely to improve.

Industrial Production- Domestic industrial output touched 16-month high at 11.7% in October 23 as compared to 6.2% in Sep 23.

Government bonds, SDL and OIS yield movements

During the past week, there were several notable changes in bond yields:

The yield for the 10-year benchmark 7.18% 2033 bond yield declined by 10 bps to 7.16%. Similarly, the 7.26% 2033 bond yield decreased by 13 bps to 7.20%. The 7.06% 2028 bond's yield lost 17 basis points to 7.07%. In the same line, the long-term paper, represented by the 7.25% 2063 bond, its yield decreased by 11 bps to 7.38%. 50-year paper, 7.46% 2073 yield decreased by 10 bps to 7.37%.

The spread between the 10-year and 5-year bonds rose to 9 bps from 2 basis points in the previous week. The spread between the 15-year benchmark and the 10-year benchmark declined to 11 bps from 14 bps. Additionally, the spread between the 30-year benchmark and the 10-year benchmark declined to 22 bps from 25 bps as compared to the previous week.

Lastly, in the Overnight Indexed Swap (OIS) rates, the 1-year OIS yield declined by 20 bps to 6.65%, while the 5-year OIS yield decreased by 25 bps to 6.20%.

We would love to hear back from you. Please Click here to share your valuable feedback,