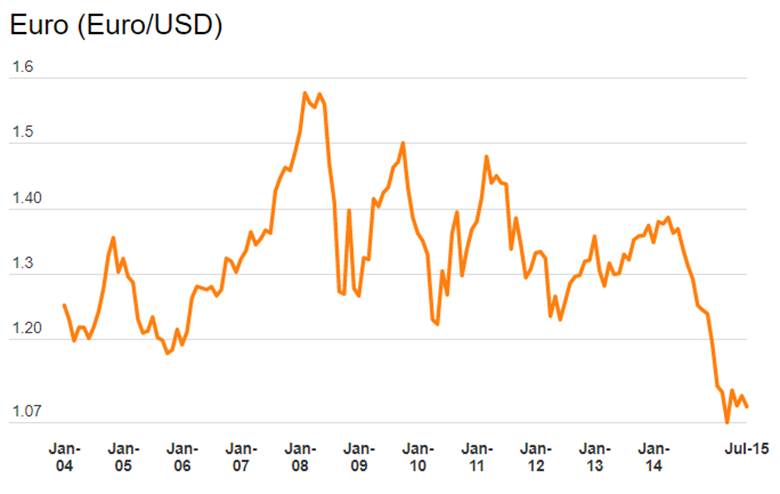

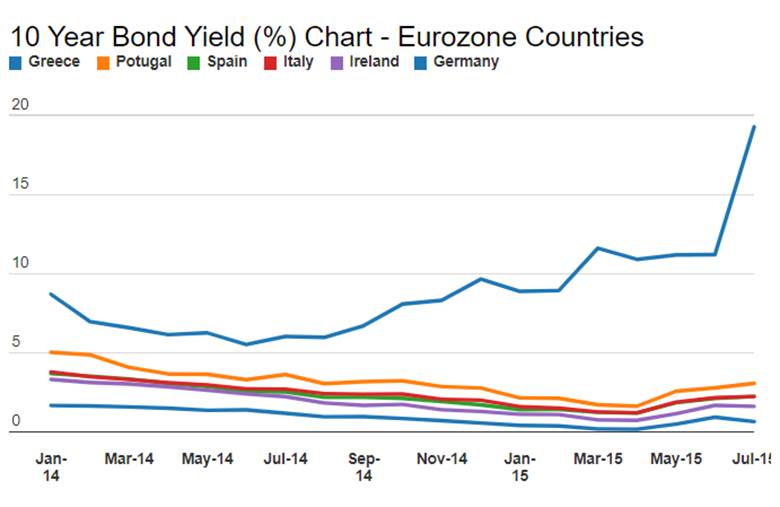

The reaction of the Euro and Eurozone bond yields has been tepid to say the least on Grexit worries. Euro fell marginally and bond yields of Spain, Italy and Portugal rose after the referendum on Sunday the 5th of July but have then stabilized. In 2011 when Grexit talk was at peaks, Euro was under tremendous pressure while bond yields of Italy, Spain and Portugal rose sharply. Charts 1 and 2.

Greece is given time till Sunday the 12th of July to come up with a debt relief proposal and if it does not pass muster, the potential for Euro exit is extremely high. If Greece exits Euro, there could be worries on the future of Euro itself but markets seem unconcerned at this point of time.

The worry now is for Greece as markets ignoring an exit would mean that any calculation of the Eurozone panicking on Grexit would have gone wrong and Greece will be completely isolated.

Markets too could well get it wrong if contagion of Grexit spreads. However with ECB ready with its warchest to buy Eurozone bonds, the markets will be wary of shorting sovereign bonds.

Hence for the people of Greece sake, the government needs to get its act right.

Bailout Extension

Greece received four months extension to its bailout package by the Euro Area Finance Ministers and has effectively given relief to markets as it will be able to meet its February 2015 commitments to its debt holders. There was much posturing by both Greece and the Euro Nations on Greece’s demand for more lenient terms on its bailout package. The markets were being led around by the prospects of Greece leaving the Euro (Grexit) but that is not on the cards at all as at this point of time, the Eurzone does not want any kind of volatility given that many countries are trying to limp back to normal after going into a recession.

The Greek general election saw the Anti Austerity party come into power with Alexis Tsipras, the leader of the Syriza Anti Austerity Party sworn in as the Prime Minister of Greece on the 26th of January 2015. The new PM promises to protect the interests of the Greek Citizens, which means renegotiating with IMF and EU on austerity terms. If Germany, the strongest country in the EU, does not agree to Greece’s demands, the country may even go out of the Euro.

Will Greece cause fresh chaos to the Euro? If Greece goes out, then countries like Portugal, Spain and Italy could follow. Will this happen at all?

The market reaction to the Greek polls was tepid. Greek ten year bond yields rose by over 80bps post elections but bond yields of Spain, Italy and Portugal stayed flat at close to record lows. Chart 1. The Euro has depreciated by close to 20% against the USD over the last nine months and is trading at eleven years lows at levels of USD 1.12 to the Euro. ECB asset purchase program of Euro 1.1 trillion announced on the 22nd of January 2015 has caused the Euro to fall, which is good for the Eurozone given its export oriented economy.

The markets are not worried about a Euro collapse as seen in 2011, when the markets tanked on worries of Greek debt default.

Financial markets have effectively isolated Greece at this point of time. Chart 1 shows that even as ten year effective benchmark Greek bond yields spiked, bonds of the indebted countries of Portugal, Ireland, Italy and Spain held steady at lower levels. Bond yields of these countries have fallen to record lows on the back of the ECB pledging to keep rates at all time lows for extended periods of

Given deflation worries in the Eurozone with January 2015 inflation being negative, there is a loosening of stance on austerity by the EU hawks. Hence, Greece could get relief even as it stays in the Euro.

time.

Athens General-Composite

Why are financial markets almost indifferent to Greece now? The reason is that after the debt restructuring by Greece in 2012, most of the Greek debt is held by the ECB, European Union (EU) and IMF. The private sector including banks holds an estimated EUR 30 billion of Greek debt. The most likely scenario is Greece defaulting once again on its debt or seeking a debt restructuring package, which would involve the private sector to take a haircut on its debt holdings.

Greece debt to GDP ratio is 175% and with the economy seeing recession for the last six years, the country is unlikely to have enough revenues to service the debt. Unemployment rate at 26% is also impacting the economy. The country grew 1.7% in the third quarter of this year but could again slip into recession if its debt problems surface again.

In 2012, at the time of restructuring, the private sector held around EUR 206 billion of Greek debt and that default fears gave rise to market volatility. This time around, the banks can easily take a haircut on its EUR 30 billion of Greek debt.