Where does a Mutual Fund Fixed Income Scheme fit into a Fixed Income Portfolio? At the accrual level, Liquid Funds, Ultra Short Funds and FMP’s can replace Fixed Deposits as they offer both liquidity on call benefits, tax benefits and at times higher returns.

When it comes to positioning for interest rate and credit spread decline, mutual funds offer the best vehicle to capture above average returns on fixed income securities. Example of positioning for interest rate and credit spread decline is given in the way we constructed our Model Fixed Income Portfolio.

We give you an example of how we constructed our Fixed Income Growth Portfolio.

Fixed Income Investment Strategy

In the Fixed Income Strategy Note released in January 2018, we positioned our strategy on rising interest rates, which have come out as per our expectations. Bond yields have risen to 3 years high levels, while yield curve has flattened at the long end. Corporate bond yield have has completely flattened for AAA bonds while credit spreads have largely risen by around 20bps. Lower rated bond spreads have stayed stable.

Given the rise in yields, rate hikes by the RBI has been factored into the yields. We had expected flat repo rate of 6% to continue through the year but RBI could start to hike rates this year if core inflation stays well above 5%. In June policy meeting RBI raised repo rate by 25 bps to 6.25%.

Domestic macro’s are strong and markets are able to withstand volatility emnating from across the globe. Inflation expectations too are kept down and this bodes well for long term bond yields. In this scenario, we are changing our portfolio by increasing duration of the portfolio through long maturity government bonds.

Investment Strategy

Gradually rising repo rate, stable inflation, comfortable liquidity and manageable macros will keep yields steady at higher levels. The yield curve will stay flat on rate hikes but will steepen as growth picks up.

Corporate bonds too will sees stability in yields, though spreads will come down on improved corporate health. Economic growth can lower spreads at the lower end of the credit rating scale.

Ideal fixed income portfolio in June 2018 will be 25% each in 10 year and 30 year government bonds, 25% in 10 year AAA rated corporate bond and 25% in lower rated corporate bonds of maturities of 3 years to 5 years.

In terms of fixed income funds, 50% in long term gilt funds, 25% in long term income funds and 25% credit risk funds.

Tax free bonds yields have come off to levels of 6.2%, which is not attractive.

The unprecedented 9 years of record low interest rates globally is coming to an end. The Fed has raised rates thrice by 25bps each in 2017 and is likely to raise rates by 75 bps in 2018 and 2019. ECB will most probably end QE in 2018 and guide for higher rates in 2019. Prospects of economic growth and inflation are looking brighter with US leading the way. US equity indices are at record highs while European indices too are trending at record highs. Commodity prices have rebounded from lows in 2016 and outlook for select industrial commodities is positive.

US treasury yields are climbing and have backed up by 150bps from lows seen in 2016. Yields in Germany have risen from negative levels. The USD had weakened from highs while emerging currencies have gained traction but over the last two months the USD has climbed due to global risk aversion.

India in the backdrop of rising interest rates globally, albeit from record lows, will be hard pressed to buck the trend though rates may not rise by much. RBI may raise the Repo Rate from 6.25% levels, the number of hikes will depend on core inflation expectations. RBI will keep liquidity easy and comfortable while the government spends to push up economic growth even as it tries to keeps down fiscal deficit.

India inflation is unlikely to go down to 4% levels but will stay within the RBI 4% +/- 2% target range. Higher global oil prices have pressured inflation but oil prices will stabilize given that oil exporting countries will increase output even as US pumps more shale oil. Improved supply as stalled projects take off will keep down inflation expectations. However as economic growth improves and output gap narrows, inflation expectations will rise. RBI has changed its policy stance from accommodative to neutral and will most probably signal the end of low interest rates in the economy.

Risk to Fixed Income Investment Strategy H2 2018

The primary risk for interest rates is sharper than expected inflation in the US leading to faster pace of Fed rate hikes, which can lead to capital outflows. Credit spreads could be affected if economic growth is weak and that will lead to rise in yields on lower rated corporate bonds.

Risk of demand and supply mismatch in government bonds exist. Banks, the largest holders of government bonds are holding bonds well in excess of statutory requirement and if they do not participate in government bond auctions and sell governments bonds if credit offtake improves, yields could trend up faster than expected.

Introduction

The ten-year government bond to repo rate spread which had fallen sharply in early 2017, on the back of demonetization and RBI rate cut expectations, has started to widen again after RBI hawkish stance on inflation in December 2017. In April policy the market saw a glimpse of hope on a dovish RBI policy but the minutes have put paid to the dovishness, with 2 RBI MPC members favoring rate hikes. The minutes have gone completely against the perceived guidance of status quo on rates for a longer period of time. In June policy meeting RBI hiked the Repo Rate by 25bps. The 25bps rate hike by the RBI lowers uncertainty for markets on the timing of the hike. Bond yields are largely factoring in multiple rate hikes and the 25bps rate hike has not moved markets by much.

10 Years G-sec Vs Repo rate (%)

What is the outlook for the bond market in H2 2018 and what should be the fixed income strategy for this year? We answer these two questions in this Fixed Income Investment Strategy Report for 2018.

What is the outlook and strategy for the bond market in H2 2018?

The year H2 2018 saw the government bond yield curve steepening Chart 2 & Chart 3 as bond yields moved up sharply on various factors such as RBI Policy, Inflation, Bond Oversupply, Concern on Fiscal Slippages and Fed Rate Hikes.

1. RBI CPI inflation target for 2018 –

Core inflation excluding HRA impact at 5.3% in April has prompted RBI to revise inflation estimates for FY 19 to 4.8% to 4.9% in H1 and 4.7% in H2, excluding HRA impact inflation is forecast at 4.6% in H1 and 4.7% in H2. RBI will consider better prospects for US and global economic growth and higher domestic economic growth when it sets the target.

2.Fed Rate Hikes – The Fed hiked rates from record lows of zero percent maintained since December 2008 for the first time in December 2015 and followed up with another 75 bps hike in 2017 and 25 bps hike in 2018. However, May 2018 policy minutes suggest Federal Reserve is not in a hurry to raise interest rates and is willing to tolerate inflation running above its 2% inflation target rate. The Fed noted that inflation in March finally hit the central bank’s goal of annual increases of 2%. The minutes called this a symmetric target, the phrase officials used to indicate that they would be comfortable letting inflation run above that 2% levels for a time, given the number of years the Fed has failed to achieve its target.

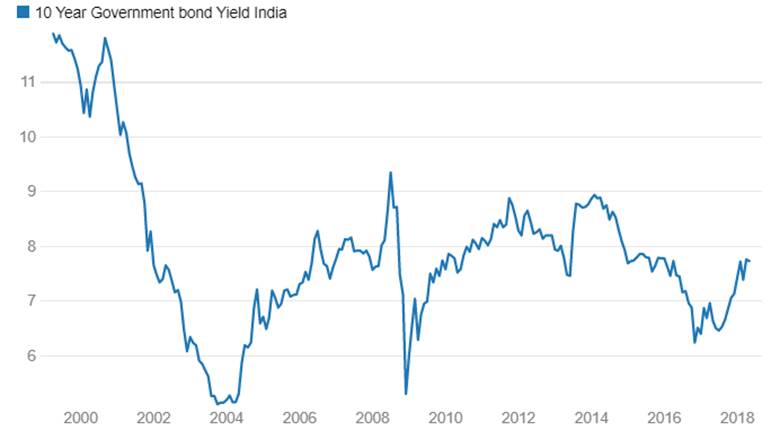

10 Year Government bond Yield India (%)

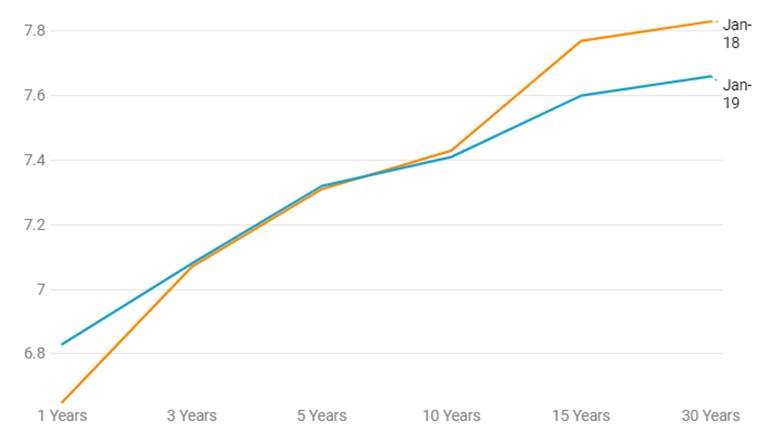

India Yield Curve (G-sec)

Inflation, Fiscal Deficit,CAD and Global Macro

Inflation Expectations

CPI inflation for April 2018 printed at 4.58% against 3.28% levels seen in March 2018 and 2.99% levels seen in April 2017. Chart 4. Core inflation printed at 5.9% in April from levels of 5.3% seen in Marc. Consumer Food Price Index (CFPI) increased 0.22% on month on month basis and increased by 2.80% year on year and against 2.81% rise in February 2018 and 0.61% rise in April 2017. Food and beverages prices rose 3.00% against 3.01% in March while Pulses prices fell 12.35% year on year. Vegetables prices rose 7.29%, weight in the index is 6.04% and Pulses and Products has 2.38% weight in the index. Clothing, footwear and housing inflation have risen by 5.11% and 8.50% respectively.Fuel and light inflation declined 49 bps in March 2018 at 5.24% against April 2017 reading. Pan,tobacco and intoxicants prices rose 7.91% yearly.

RBI’s medium-term CPI target is 4% but given government will spend more on infrastructure & wanted to increase rural income which will lead to both higher borrowings and higher inflation on the back of consumption demand. and that global economies are expected to do better, which could take up select commodity prices. In Budget also government has shown a spend of over 20% on infrastructure and has kept down total expenditure growth to 10.1% year on year. The government has also shown higher spends for Rural infrastructure, which is expected to grow rural incomes in the next few years. to rural growth

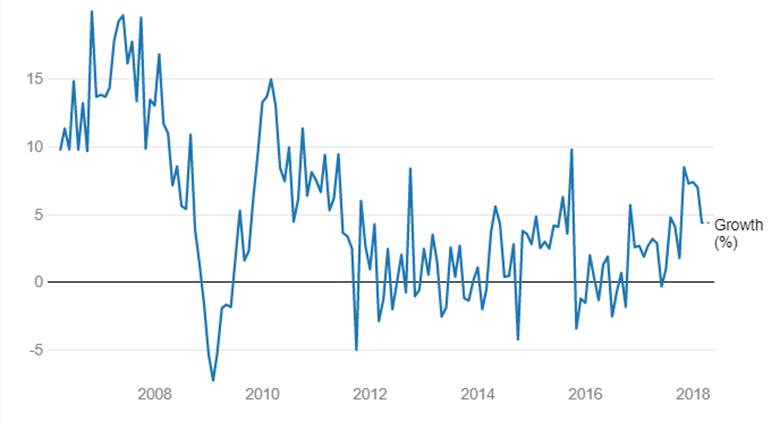

India’s index of industrial production rose by 4.3% in the April-March 2018 period against 4.6% seen last year, Industrial production has struggled due to double whammy from Demonetisation and implementation of GST. However going forward industrial production is expected to do well as industry has come out from the shock of demonetisation, improvement in consumer demand and the government is working hard to end GST glitches Chart 5

India’s economy is expected to grow at levels of around 7.5% from 6.6% in the last fiscal. Chart 6 Economic growth would revive in 2018-19 on government spending and improved global economic growth. Exports have started to show a positive trend since September 2016 (except October 2017 & March 2018 data) which indicate improvement in global trade conditions. Global Economy is also expected to grow at 3.1% in 2018.

CPI Inflation (%) Y-o-Y

Index Of Industrial Production

India GDP growth rates (%)

Fiscal Deficit and Demand Supply of Government Bonds

Government of India in consultation with the RBI has deviated from its stance of front loading borrowing in the first half of every fiscal year. In the fiscal year 2018-19, the government will borrow 47.56% of total budgeted borrowing in the April-September 2018-19 period, against borrowing of over 60% seen in the previous fiscal years. Government will also issue short maturity bonds and floating rate bonds as part of its borrowing. Government borrowing for the first half of 2018-19 is easily achievable if there are no major disruptions in the market.Bond redemption worth Rs 875.68 billion will help borrowing go through smoothly. Net borrowing is around Rs 2004.32 billion in the first half which is 13.71% lower than the borrowing seen in the first half of fiscal 2017-18.

The Government intends to use inflows from Small Savings Schemes to fund its Fiscal Deficit. The Government will borrow Rs 1000 billion from NSSF as against budgeted amount of Rs 750 billion.The Government also plans to issue more Floating Rate Bonds (FRBs) and CPI linked bonds, upto 10% of issuances during the year. FPI limits will be raised in FY19.

The government has projected a fiscal deficit of 3.3% of GDP for the fiscal year 2018-19 from a fiscal deficit of 3.5% of GDP for the fiscal year 2017-18. The government should control its fiscal deficit if it wants interest rates to stay stable in the economy. The reason is that banks have upped their investments in government bonds post demonetisation. Investments have grown by 9% as of March 2018, year on year, against growth of 15% seen last year. Banks are already holding bond well above the SLR rate of 19.5% (as of January 2018) at levels of 28%. Demand from banks for government bonds will be low in this fiscal year.